Original Article – February 22, 2016 by Allard Ferwerda

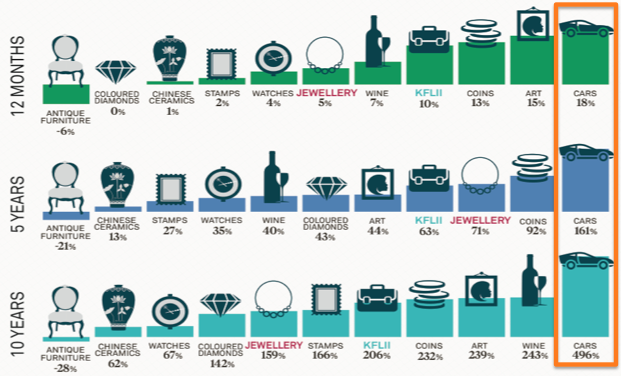

The fact of the matter is that prices for rare classic cars have been recovering quite impressively since the early 1990’s collapse in the market. We have seen a big rise in prices for these cars: On average more than + 480 % YTD January 2016 over a ten year period and +83% YTD January 2016 over a 3 year period (this does not include costs for storage, maintenance, insurance etc.)

Source: Knight Frank: Luxury Investment Index Q3 2015, p. 3

This implies a long term outperformance of many traditional asset classes and their respective indices by far. Although this would be comparing ‘apples with oranges’ and does not even take the fun factor into consideration it is without any doubt that, with current low interest rates, economic uncertainty and volatile stock markets, it is still a good alternative to invest in. In this article I will, however, not elaborate about the pro’s and con’s of these so-called passion investments. Both advocates and opponents already know them and many articles have been published about this topic. I do want to question however whether the classic car market will continue to be a bull market or whether it will turn into a bear market.

From an auction perspective, only representing a small part of all classic car transactions which i will explain later, we noticed some ‘cracks in the ice ‘over 2015. Summarised the story is, despite some individual peaks, one of consolidation, oversupply of many ‘blue chip’ collectibles and too many auctions (e.g. cramming four major European auctions into just over a week in september 2015 is a recipe for disaster!). With regards to the latter the auction figures speak for itself. Comparing both six-month periods in 2015, the percentage of cars sold below low estimate from January to June 2015 was 46%. This increased to 54% for the rest of 2015. For cars sold above top estimate, a figure of 20% slipped to 13% by December 2015, and by that month 75% of lots failed to beat their mid- estimate values. Looking at this it could indicate that we are heading towards a bear market and this is what we lately have been reading in the media. Classic Car guru Simon Kidston commented about the most recent 2016 auction at Rétromobile 2016 by ARTCURIAL that:

“Aside from the two iconic Ferraris, both from French deceased estates, not much has prompted the “Where did they find that?” which greets the discoveries we all dream about. You could question the wisdom of offering quite so much average, pseudo-collector fodder in such a short space of time: the sight of six Ferrari Testarossas (picture below), all red, lined up at one auction waiting optimistically for buyers probably summed up much of what’s wrong with the recent bull market”.

Source: k500.com / Simon Kidston

Although this certainly could be considered as the right conclusion from an auction perspective the mainstream and financial media is, in general, too much focussed on this relatively small area of the market and are generalising their conclusions for the overall market. Please note that (at least in in Europe) the majority of all classic car sales transactions in 2015 were made outside classic car auctions! This is generally ignored, simply because data of private transactions aren’t readily available. If you talk to classic car experts that act on behalf of collectors and investors they will tell you that most of the exquisite classic cars never even make it onto the open market. A good example of this was the most expensive car ever sold in private transaction in October 2013: a 1963 Ferrari 250 GTO (chassis number 5111GT) sold for USD 52m.

So what does this all mean for the outlook for the remainder of 2016? will the recent bull market turn into a bear market? Although I don’t have a crystal-ball various car experts advocate that buyer confidence still remains, mainly because they have seen a vast number of enquiries over the past two months and most speculators have largely left the market. Personally I do not believe we are heading towards a further steep growth of the recent bull market and neither to a bear market. The verdict would, from my point of view, be the following:

1. The overall market will continue to grow but, other than the ‘top-end’, most increases will be at a slower rate:

- Although buyers confidence is still high collectors, drivers and investors do not want to take the risk to pay a perceived high price for ‘blue chip’ collectables and are now looking for alternative targets.

- Highly-priced, lower-quality cars will remain in stock (e.g. an overkill of low quality porsche 911’s)

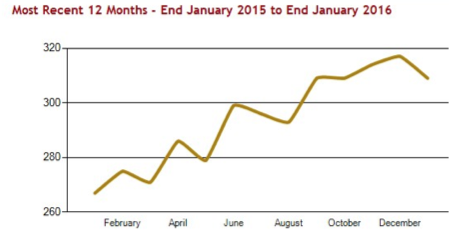

- A lower turnover and more cautious buying was also reflected in January’s HAGI Top index performance (YTD January 2016: -2.5% or a decrease from 317.38 to 309.45).

Source: HAGI newsletter February 2016

2. The gap between ‘top-end’ classics and the rest will further increase:

- Sales prices of the most expensive classics (over €6m) will continue upwards .They are now being treated more as works of art: pedigree and certification is key

3. Supported by the “generational factor” the gap, as mentioned under bullet #2., will result in a two tier shift in demand for the rest:

- From cars of the 50’s, 60’s and early 70’s to cars of the end 70’s, 80’s and early 90’s

- To rare modern hypercars (‘TO BE’ classics) such as Ferrari Enzo, LaFerrari, Porsche 918, Bugatti Veyron etc.

I expect that, for low volume models, this will be reflected in a further increase in prices for both segments

4. Rather than the oversupply of ‘over restored’ cars demand for unrestored original cars in a good to decent condition with a ‘soul’ (patina, scent etc.) will further increase and hence their prices

5. Rising prices saw some (volume) models flood the market in 2015:

- Porsche 930 Turbo’s > 1977 and post Enzo era Ferraris such as the Testarossa are a good example

- It is expected that prices for these ‘volume models’ will slightly decrease over the coming months

6. Manufacturers’ heritage operations will increase:

- Porsche, Mercedes-Benz, Ferrari and Jaguar are leading the way with heritage operations. Serious money can be made from their history, and it could even help them sell modern cars

- You can expect to see more ‘re-releases’ in 2016 and onwards, following Jaguar’s success with the light weight E-Type

DISCLAIMER

The elements contained in this opinion have been prepared solely for the purpose of information and do not constitute an advise to buy or sell a car. While particular attention has been paid to the contents of this opinion, no guarantee, warranty or representation, express or implied, is given to the accuracy, correctness or completeness thereof.

Any information given in this opinion may be subject to change or update without notice. The publisher can not be held direct or indirect liable or responsible with respect to the information and/or recommendations of any kind expressed herein.